JANUARY 2004

The mathematics of human thought

This year marks the 150th anniversary of the publication of the book that set the scene for the introduction of the computer a century later: George Boole’s The Laws of Thought, first published in 1854. The dramatic breakthrough that the book represented is reflected today in our use of the terms “boolean logic” or “boolean algebra” to mean the combination of ideas using the operations AND, OR, and NOT, and our use of the term “boolean search” to mean a database or Web search involving combinations of key words using AND, OR, and NOT. (The fact that we generally do not capitalize “boole” in those contexts indicates just how pervasive Boole’s influence has been.)

Boole’s book begins with these words:

The design of the following treatise is to investigate the fundamental laws of those operations of the mind by which reasoning is performed; to give expression to them in the symbolic language of a Calculus, and upon this foundation to establish the science of Logic and construct its method.

By the phrase “the symbolic language of a Calculus” Boole meant algebra. Not just the use of algebraic symbols like x, y, z, p, q, r to denote unknown words, phrases, or propositions. That much had been done by the logicians of ancient Greece. What Boole was talking about was using the entire apparatus of the high school algebra class, with operations such as addition and multiplication and the employment of methods to solve equations. Boole’s algebra required the formulation of a symbolic language of thought. Solving an equation in that language would not lead to a numerical answer; it would give the conclusion of a logical argument. His algebra was to be an algebra of thought.

Even today, in the twenty-first century, when we are familiar with computers—the “thinking machines” that are direct descendants of Boole’s logical algebra—it seems an audacious idea to write down algebraic equations that describe the way we think. What led Boole to propose such a thing, and why did he think it might be successful?

George Boole was born in England in 1815. Though the world was to regard him as a mathematician—indeed, as one of the most influential mathematicians of all time—he shared his interests between mathematics and psychology. Were he alive today, he would undoubtedly refer to himself as a cognitive scientist, a term that was first used in the early 1950s. He was largely self taught, and it may have been the absence of a teacher to lead him away from such a seemingly nonsensical idea that enabled him to seek to capture the patterns of thought by means of algebra. The mark of his genius is that he succeeded to such an extent.

Boole first published his algebra of thought in 1847 in a small pamphlet entitled The Mathematical Analysis of Logic. The simplest way to describe the contents of this pamphlet is to quote from the opening section.

They who are acquainted with the present state of the theory of Symbolic Algebra, are aware that the validity of the processes of analysis does not depend upon the interpretation of the symbols which are employed, but solely upon the laws of their combination. Every system of interpretation which does not affect the truth of the relations supposed, is equally admissible, and it is thus that the same processes may, under one scheme of interpretation, represent the solution of a question on the properties of number, under another, that of a geometrical problem, and under a third, that of a problem of dynamics or optics. … It is upon the foundation of this general principle, that I purpose to establish the Calculus of Logic …

It is worth reading through the above passage a second time. Boole made every word count.

As a result of his new algebra of logic, in 1849 Boole was appointed to the chair of mathematics at the newly founded University College, Cork. As soon as he had established residence in Ireland, he began work on a larger book about his new theory. He was particularly keen to ensure that his mathematics really did capture laws of mental activity, and to this end he spent a great deal of time reading psychological literature and familiarizing himself with what the philosophers had to say about mind and logic.

He used his own money and that of a friend to publish his second, more substantial book on his ideas in 1854. Its full title was An Investigation of the Laws of Thought on Which are Founded the Mathematical Theories of Logic and Probabilities. but it is generally referred to more simply as The Laws of Thought. By and large, the only substantial difference between the 1854 book and the earlier pamphlet of 1847 was the addition of his treatment of probability, using his new algebraic framework. The logic itself was largely unchanged.

Boole’s idea was to try to reduce logical thought to the solution of equations—a logical holy grail ever since the German mathematician Gottfried Leibniz had tried to do it in the 17th century. Leibniz attempted to develop an “algebra of concepts”, in which algebraic symbols had denoted concepts, such as big, red, man, woman, unicorn, but he had met with only limited success.

Boole wanted his algebra to encompass all of Aristotle’s insights into human reasoning (the famous Greek “All men are mortal” syllogisms) as well as the Stoics’ logic of propositions (what we now refer to as propositional calculus). He took his symbols x, y, z, etc. to denote arbitrary collections of objects. For example, the collection of all men, the collection of all mortals, the collection of all bankers, or the collection of all natural numbers. He then showed how to do algebra with symbols that denote collections—to write down and solve equations—in a way that corresponds to performing logical deductions.

In order to be able to write down and solve algebraic equations involving collections, Boole had to define what it meant to add and to multiply two collections. Since his algebra was intended to capture some of the patterns of logical thought, his definitions of addition and multiplication had to correspond to some basic thought processes. Moreover, it would be easier to do algebra if he could define addition and multiplication in such a way that they had many of the familiar properties of addition and multiplication of numbers, making his new algebra of thought similar to the algebra everyone was used to.

Here is what he did. Given collections x and y, Boole denoted the collection of objects common to both x and y by xy. For example, if x is the collection of all Germans and y is the collection of all sailors, then xy is the collection of all German sailors.

Boole’s definition of addition was more complicated than it needed to be, so other mathematicians of the time modified it to the following simple idea: x + y is the collection of objects that are in either x or y or both. For example, if x is the collection of all red pens and y is the collection of all blue pens, then x + y is the collection of all pens that are either red or blue.

With these definitions of multiplication and addition, Boole’s system had the following properties:

x + y = y + x

xy = yx

x + (y + z) = (x + y) + z

x(yz) = (xy)z

x(y + z) = xy + xz

These equations should look familiar for ordinary arithmetic, where the letters denote numbers. They are the two commutative laws, the two associative laws, and the distributive law. Because of the similarities between Boole’s algebra of collections and ordinary arithmetic, Boole was able to perform calculations in his system, i.e., algebraic manipulations such as solving equations. However, solving an equation in Boole’s system corresponds not to arithmetic but to logical reasoning about … well, about whatever the symbols are taken to mean—men, women, unicorns, what to prepare for dinner, etc. True, solving Boolean equations is not necessarily the best way to make a human decision. But the point was that patterns of logical thought could be represented by means of algebra. How far that would get you in real life was a question for later generations to take up.

There are further similarities between Boole’s system and ordinary algebra. For instance, in ordinary arithmetic the number 0 is special: adding 0 to any number leaves the number unchanged. In order for his algebra to work, Boole also needed a zero. He obtained it by taking 0 to be the empty collection.

One advantage of having a 0 is that it provides a way to write down an algebraic equation saying that various things do not exist. For example, in Boole’s algebra we can express the fact that unicorns do not exist by letting x be the collection of all unicorns and writing down the equation x = 0.

With 0 defined as the empty collection, the symbol 0 has the same special properties in Boole’s algebra of collections as it does in ordinary algebra:

x + 0 = x

x0 = 0

for any collection x.

Although Boole’s algebra had many of the properties of ordinary algebra, it was not exactly the same. Boole really did have to work with a strange, new kind of algebra. For instance, in Boole’s algebra, the following two equations are true:

x + x = x

xx = x

These equations are certainly not true for ordinary arithmetic.

Incidentally, the axiomatic system that today’s mathematicians refer to as a “boolean algebra” is not due to Boole. Rather, it was developed by other mathematicians who built on Boole’s original work.

By reducing reasoning to doing algebra, Boole opened up the possibility of building a reasoning machine. Even today, it is hard to imagine any kind of mechanical or (these days) electronic machine being able to reason the way humans do about, say, local politics. What can a machine possible know about local government? On the other hand, even in Boole’s day it seemed perfectly possible to construct a machine that could manipulate algebraic symbols according to some general rules.

Indeed, the rules Boole presented for manipulating algebraic expressions and for solving equations in his system were sufficiently mechanical that the English logician W. S. Jevons was able to use them to build a mechanical reasoning machine which he demonstrated to the Royal Society in 1870. Not surprisingly, given the prevailing technology at the time, Jevons’ device looked for all the world like an old style mechanical cash register. But for all its antiquated appearance, as an implementation of logic it was a stunning early ancestor of the modern electronic computer.

Today’s electronic computer is, at heart, just an implementation in silicon of Boole’s algebra of thought, with streams of electrons performing Boole’s algebraic operations. The OR gates and AND gates you can read about in books that describe how computers work correspond directly to Boole’s algebraic operations of addition and multiplication. In last month’s column I described how the mathematician John von Neumann played a key role in the the design of one of the first electronic computers in the early 1950s. It was the theoretical work of George Boole a century earlier that prepared the foundations upon which von Neumann and this colleagues helped usher in today’s computer era.

NOTE: This months’ column is abridged from my book Goodbye Descartes: The End of Logic and the Search for a New Cosmology of the Mind, published by John Wiley in 1997. For more on George Boole, and the development of logic and its role in the invention of the modern computer, consult that book.

For more in-depth coverage of the use of language in mathematics, but still at an elementary level, see my book Sets, Functions, and Logic, the Third (completely revised) Edition of which has just been published by Chapman and Hall.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin ( devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and “The Math Guy” on NPR’s Weekend Edition. His most recent book is The Millennium Problems: The Seven Greatest Unsolved Mathematical Puzzles of Our Time, published by Basic Books (hardback 2002, paperback 2003).

FEBRUARY 2004

The Archimedes Cattle Problem

In the third century BC, the famous Greek mathematician Archimedes issued a challenge to the Alexandrian mathematicians, headed by Eratosthenes. Written in the form of an epigram, Archimedes’s challenge begins thus:

“Compute, o friend, the number of oxen of the Sun, giving thy mind thereto, if thou has a share of wisdom.”

He then goes on to describe, in wonderfully poetic language, a certain herd of cattle, consisting of four types, with bulls and cows of each type. The number of cattle in each of the eight categories is not given, but these numbers are related by nine simple conditions which Archimedes spells out. For example, one of these conditions is that the number of white bulls is equal to the number of yellow bulls plus five-sixths of the number of black bulls. The problem is to determine the number of cattle of each category, and thence the size of the herd. (Actually, what is required is the smallest possible number, since the nine conditions do not imply a unique answer. I’ll give the actual problem in a moment.)

In his epigram, Archimedes goes on to say that anyone who solves the problem would be “not unknowing nor unskilled in numbers, but still not yet to be numbered among the wise.” Nothing could be more apt, since there was to elapse 2,000 years before a computer finally found the solution. Clearly Archimedes had a mischievous streak in addition to his principles, and was trying to pull a fast one on his Alexandrian rivals.

In 1880, a German mathematician called Amthor showed that the total number of cattle in Archimedes herd had to be a number with 206,545 digits, beginning with 7766. Not surprisingly, Amthor gave up at that point. Over the next 85 years, a further 40 digits were worked out. But it was not until 1965 when mathematicians at the University of Waterloo in Canada finally found the complete solution. It took over seven and a half hours of computation on an IBM 7040 computer. Unfortunately, no one thought to keep the printout of the answer! The world had to wait until the problem was solved a second time using a Cray-1 computer in 1981 for a published printout. It took the Cray just 10 minutes to crack it. But after 2,000 years I think Archimedes has to have the last laugh.

So what is Archimedes’ Cattle Problem?

Archimedes asks you to imagine a certain herd of cattle consisting of both cows and bulls, each of which may be white, black, yellow, or dappled. The numbers of each category of cattle are connected by various, simple conditions. To give these, let W denote the number of white bulls, w the number of white cows, B the number of black bulls, b the number of black cows, with Y, y and D, d playing analogous roles for the other colors. Using Archimedes’ method of writing fractions (that is, utilizing only simple reciprocals), the fist seven conditions which these various numbers have to satisfy are:

(1) W = (1/2 + 1/3)B + y

(2) B = (1/4 + 1/5)D + Y

(3) D = (1/6 + 1/7)W + Y

(4) w = (1/3 + 1/4)(B + b)

(5) b = (1/4 + 1/5)(D + d)

(6) d = (1/5 + 1/6)(Y + y)

(7) y = (1/6 + 1/7)(W + w)

The two remaining conditions are:

(8) W + B is a perfect square

(9) Y + D is a triangular number.

[A triangular number is one that is equal to a number of balls that may be arranged to form a triangle, which is the same as saying that the number must be of the form n(n+1)/2 for some n.]

The problem is to determine the size of the eight unknowns, and thus the size of the herd. More precisely, the aim is to find the least solution, since the conditions admit more than one solution. If conditions (8) and (9) are dropped, the problem is relatively easy. The smallest herd consists of 50,389,082 cattle. The additional two conditions make the problem considerably harder. It has been claimed that the first complete solution was worked out by the Hillsboro (Illinois) Mathematics Club between 1889 and 1893, although no copy of their solution has ever been found, and there is some evidence to suggest that what they in fact did was work out some of the digits of the 206,545 digit solution and provide an algorithm for the computation of the remainder.

In 1965, H. C. Williams, R. A. German, and C. R. Zarnke at the University of Waterloo in Canada used an IBM 7040 computer to crack the problem once and for all. The final solution occupied 42 sheets of print-out. In 1981, Harry Nelson repeated the calculation using a Cray-1. This machine took a mere 10 minutes to come up with the answer. Reduced to fit 12 pages of print-out on a single journal page, the solution was published in the Journal of Recreational Mathematics 13 (1981), pp.162-176.

The Math Guy on NPR radio

I often get emails from math instructors who want to locate one of my “Math Guy” conversations with host Scott Simon on NPR’s Weekend Edition. The Math Guy slot has been on the air since 1996 (although the name “Math Guy” did not come until later), on an irregular basis, and to date there have been 34 such segments. Since 1998, NPR has made the sound files available on its website. For a complete list, with links, go to http://profkeithdevlin.com/MathGuy.html.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin (Email: devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and “The Math Guy” on NPR’s Weekend Edition. His most recent book is The Millennium Problems: The Seven Greatest Unsolved Mathematical Puzzles of Our Time, published by Basic Books (hardback 2002, paperback 2003).

MARCH 2004

A Year of Anniversaries

The year 2004 sees an unusually large number of anniversaries of major advances in mathematics. I began the year with my January column devoted to one of those anniversaries: It is exactly 150 years since the publication in 1854 of George Boole’s major work The Laws of Thought. But that merely scratched the surface of this bumper anniversary year.

350 years: In an exchange of five letters in 1654, Pierre De Fermat and Blaise Pascal founded modern probability theory.

250 years: In 1754, Joseph-Louis Lagrange made important discoveries about the tautochrone, which in due course would contribute substantially to the new subject of the calculus of variations.

200 years: In 1804, Wilhelm Bessel published a paper on the orbit of Halley’s comet, based on observations by Thomas Harriot 200 years earlier.

150 years: Three major developments took place in 1854. In addition to Boole’s publication of The Laws of Thought in England, Arthur Cayley (also in England) made the first attempt to define an abstract group, while in Germany Bernhard Riemann completed his Habilitation. In his dissertation, Riemann studied the representability of functions by trigonometric series and gave the conditions for a function to have an integral (what we now call “Riemann integrability”). In a lecture titled On the hypotheses that lie at the foundations of geometry, given on 10 June 1854, he defined an n-dimensional space and gave a definition of what is today called a “Riemannian space”.

100 years: In 1904, Henri Poincare came within a whisker of discovering relativity theory. In an address to the International Congress of Arts and Science in St Louis, he remarked that observers in different frames will have clocks which will “… mark what one may call the local time. … as demanded by the relativity principle the observer cannot know whether he is at rest or in absolute motion.” Unfortunately, he never took the next step—the full Principal of Special Relativity—leaving the field open for Albert Einstein to make that important leap forward and claim the credit the following year.

I’ll take a look at some of these major advances in future columns. This month, I want to look in depth at the oldest one: the Fermat-Pascal correspondence that established modern probability theory. My account is taken from my book The Language of Mathematics.

Figuring the odds

The first step toward a theory of probability came when a sixteenth century Italian physician—and keen gambler—called Girolamo Cardano described how to give numerical values to the possible outcomes of the roll of dice. He wrote up his observations in a book titled Book on Games of Chance, which he published in 1525.

Suppose you roll a die, said Cardano. Assuming the die is “honest”, there is an equal chance that it will land with any of the numbers 1 to 6 on top. Thus, the chance that each of the numbers 1 to 6 ends face up is 1 in 6, or 1/6. Today, we use the word “probability” for this numerical value: We say that the probability that the number 5, say, is thrown is 1/6.

Going a step further, Cardano reasoned that the probability of throwing either a 1 or a 2 must be 2/6, or 1/3, since the desired outcome is one of two possibilities from a total of six.

Going further still—though not quite far enough to make a real scientific breakthrough—Cardano calculated the probabilities of certain outcomes when the die is thrown repeatedly, or when two dice are thrown at once.

For instance, what is the probability of throwing, say, a 6 twice in two successive rolls of a die? Cardano reasoned that it must be 1/6 times 1/6, that is, 1/36. You multiply the two probabilities since each of the six possible outcomes on the first roll can occur with each of the six possible outcomes on the second roll, that is, 36 possible combinations in all. Likewise, the probability of throwing, say, a 1 or a 2 twice in two successive rolls is 1/3 times 1/3, namely 1/9.

What is the probability that, when two dice are thrown, the two numbers showing face up will add up to, say, 5? Here is how Cardano analyzed that problem. For each die, there are six possible outcomes. So there are 36 (= 6 x 6) possible outcomes when the two dice are thrown: each of the six possible outcomes for one of the two dice can occur with each of the six possible outcomes for the other. How many of these outcomes sum to 5? List them all: 1 and 4, 2 and 3, 3 and 2, 4 and 1. That’s four possibilities altogether. So of the 36 possible outcomes, 4 give a sum of 5. So, the probability of a sum of 5 is 4/36, that is, 1/9.

Cardano’s analysis provided just enough for a prudent gambler to be able to bet wisely on the throw of the dice—or perhaps be wise enough not to play at all. But Cardano stopped just short of the key step that leads to the modern theory of probability. So too did the great Italian physicist Galileo, who rediscovered much of Cardano’s analysis early in the seventeenth century, at the request of his patron, the Grand Duke of Tuscany, who wanted to improve his performance at the gambling tables. What stopped both Cardano and Galileo was that they did not look to see if there was a way to use their numbers—their probabilities—to predict the future.

That key step was left to the two French mathematicians Blaise Pascal and Pierre de Fermat. In 1654, the two exchanged a series of five letters (the last was dated 27 October) that most people today agree was the beginning of the modern theory of probability. Though their analysis was phrased in terms of one specific problem about gambling, Pascal and Fermat developed a general theory that could be applied in a wide variety of circumstances, to predict the likely outcomes of various courses of events.

The problem that Pascal and Fermat examined in their letters had been around for at least two hundred years: How do two gamblers split the pot if their game is interrupted part way through? For instance, suppose the two gamblers are playing a best-out-of-five dice game. In the middle of the game, with one player leading two to one, they have to abandon the game. How should they divide the pot?

If the game were tied, there wouldn’t be a problem. They could simply split the pot in half. But in the case being examined, the game is not tied. To be fair, they need to divide the pot to reflect the two-to-one advantage that one player has over the other. They somehow have to figure out what would most likely have happened had the game been allowed to continue. In other words, they have to be able to look into the future—or in this case, a hypothetical future that never came to pass.

The problem of the unfinished game seems to have first appeared in the fifteenth century, when it was posed by Luca Paccioli, the monk who taught Leonardo de Vinci mathematics. It was brought to Pascal’s attention by Chevalier de Mere, a French nobleman with a taste for both gambling and mathematics. Unable to resolve the puzzle on his own, Pascal asked Fermat—widely regarded as the most powerful mathematical intellect of the time—for his help.

In their letters, Pascal and Fermat not only solved the puzzle of the unfinished game, but in so doing they established the foundations of modern probability theory.

To arrive at an answer to Pacciola’s puzzle, Pascal and Fermat examined all the possible ways the game could have continued, and observed which player won in each case. For instance, in the case of the best-of-five dice game that is stopped after the third round with one player in the lead by two to one, there are four possible ways the game can be completed. Of those four, three are won by the player in the lead after the third round. So the two players should split the pot with 3/4 going to the person in the lead and 1/4 going to the other.

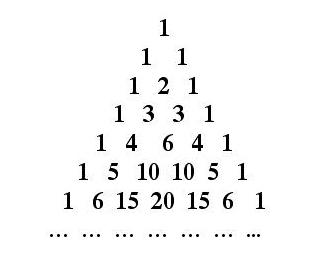

Alhough Pascal and Fermat developed the theory of probability collaboratively, through their correspondence—the two men never met—they each approached the problem in different ways. Fermat preferred the algebraic techniques that he used to such devastating effect in number theory. Pascal, on the other hand, looked for geometric order beneath the patterns of chance. That random events do indeed exhibit geometric patterns is illustrated in dramatic fashion by what is now called Pascal’s triangle, shown here.

The symmetrical array of numbers shown in the figure is constructed according to the following simple procedure.

At the top, start with a 1.

On the line beneath, put two 1s.

On the line beneath that, put a 1 at each end, and in the middle the sum of the two numbers above and to each side, namely 1 + 1 = 2.

On line four, put a 1 at each end, and at each point midway between two adjacent numbers on line three put the sum of those numbers. Thus, in the second place you put 1 + 2 = 3 and in the third place you put 2 + 1 = 3.

On line five, put a 1 at each end, and at each point midway between two adjacent numbers on line four put the sum of those numbers. Thus, in the second place you put 1 + 3 = 4, in the third place you put 3 + 3 = 6, and in the fourth place you put 3 + 1 = 4.

By continuing in this fashion as far as you want, you generate Pascal’s triangle. The patterns of numbers in each row occur frequently in probability computations—Pascal’s triangle exhibits a geometric pattern in the world of chance.

For example, suppose that when a married couple have a child, there is an equal chance of the baby being male or female. (This is actually not quite accurate, but it’s close.) What is the probability that a couple with two children will have two boys? A boy and a girl? Two girls? The answers are, respectively, 1/4, 1/2, and 1/4. Here’s why. The first child can be male or female, and likewise the second. So we have the following four possibilities (in order of birth in each case): boy-boy, boy-girl, girl-boy, girl-girl. Each of these four possibilities is equally likely, so there is a 1-in-4 probability that the couple will have two boys, a 2-in-4 (i.e., 1/2) probability of having one of each gender, and a 1-in-4 probability of having two girls.

Here is where Pascal’s triangle comes in. The third line of the triangle reads 1 2 1. The sum of these three numbers is 4. Dividing each number on the row by the sum 4, we get (in order): 1/4, 2/4 (= 1/2), 1/4, the three probabilities for the different kinds of family.

Suppose the couple decide to have three children. What are the probabilities that they have three boys? Two boys and a girl? Two girls and a boy? Three girls? The fourth row of Pascal’s triangle gives the answers. The row reads: 1 3 3 1. These numbers sum to 8. The different probabilities are, respectively: 1/8, 3/8, 3/8, 1/8.

Similarly, if the couple has four children, the various possible gender combinations have probabilities 1/16, 4/16, 6/16, 4/16, 1/16. Simplifying these fractions, the probabilities read: 1/16, 1/4, 3/8, 1/4, 1/16.

In general, whenever there is an event where the individual outcomes can occur with equal probability, Pascal’s triangle gives the probabilities of the different possible combinations that can arise when the event is repeated a fixed number of times. If the event is repeated N times, you look at the N+1’st row of the triangle, and the numbers in the row give the numbers of different ways each particular combination can arise. Dividing the row numbers by the sum of the numbers in the row then gives the probabilities.

Since Pascal’s triangle can be generated by a simple geometric procedure, this method shows that there is geometric structure beneath questions of probability. It’s discovery was a magnificent achievement.

Addendum to last month’s column

Last month, I discussed the Archimedes cattle problem, oberving that, in 1981, Harry Nelson solved the problem in ten minutes on a Cray-1 supercomputer. Stan Wagon wrote to point out that algorithms have improved since then. According to Wagon, a good modern laptop can solve the problem in about a second using Mathematica. A section is devoted to this in Wagon and Bressoud’s book A Course In Computational Number Theory. Section 7.5 of the book is titled “Archimedes and the Sun God’s Cattle”. Solving the basic equation (a Pell equation) involved takes 0.01 seconds, but then you have to go through a While loop to get the right solution, and that takes 0.07 seconds.

Wagon also notes that some ideas of Ilan Vardi allow an even faster approach that requires almost no computation. Vardi’s work is detailed in his paper Archimedes’ Cattle Problem,American Mathematical Monthly 105 (1998) 305-319.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin (Email: devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and “The Math Guy” on NPR’s Weekend Edition. For a complete list of Math Guy segments, with links, go to http://www- csli.stanford.edu/~devlin/MathGuy.html

Devlin’s most recent book is The Millennium Problems: The Seven Greatest Unsolved Mathematical Puzzles of Our Time, published by Basic Books (hardback 2002, paperback 2003).

APRIL 2004

The Abel Prize Awarded: The Mathematicians’ Nobel

The Abel Prize, established by the Norwegian government in 2001 as an annual “Nobel Prize for Mathematics” and first awarded last year, will go this year to Professor Isadore Singer, 80, of MIT and Sir Michael Atiyah, 75, who has held an honorary position at the University of Edinburgh since he retired from Cambridge University a few years ago.

The prize is being given for the work that led to the names Atiyah and Singer being forever linked in the field of mathematics: the “Atiyah-Singer Index Theorem”, which they formulated and proved in a series of papers they published in the early 1960s. The Index Theorem provides a bridge between pure mathematics (differential geometry, topology, and analysis) and theoretical physics (quantum field theory) that has led to advances in both fields.

The Norwegian Academy of Science, which oversees and manages the new prize, referred to the Index Theorem as “one of the great landmarks of 20th century mathematics”. In fact, it is no exaggeration to say that the result changed the landscape of mathematics. Atiyah, who trained as an algebraic geometer and topologist, and Singer, who came from analysis, worked on ramifications of the theorem for twenty years.

Sir Michael, quoted in an article in Britain’s Daily Telegraph newspaper (March 26) commented: “the Index Theorem provides a Trojan horse that mathematicians have used to get into physics and vice versa. When we first did it, we had no inkling that this would follow.”

Singer, speaking to BBC News (March 26), said: “I am delighted to win this prize with Sir Michael. The work we did broke barriers between different branches of mathematics and that’s probably its most important aspect. … It has also had serious applications in theoretical physics.” Referring to the creation of the Abel Prize, he added “I appreciate the attention mathematics will be getting. It’s well-deserved because mathematics is so basic to science and engineering.”

Atiyah and Singer will receive their award from Norway’s King Harald at a ceremony in Oslo on May 25.

The prize amount is 6 million Norwegian Kroner, currently about $875,000. The award of the first Abel Prize, made in 2003 with relatively little fanfair outside of Scandinavia, went to the French mathematician Jean-Pierre Serre for his work in algebraic geometry and number theory.

The Abel Prize

There is no Nobel Prize for mathematics, but many mathematicians have won the prize, most commonly for physics but occasionally for economics, and in one case for literature. For instance, when mathematician John Nash won a Nobel Prize in 1994, it was for a result that had a major impact in economics. (Nash’s achievement was celebrated in director Ron Howard’s 2002 movie A Beautiful Mind, starring Russell Crowe.)

The Abel Prize is intended to give the mathematicians their own equivalent of a Nobel Prize. Such an award was first proposed in 1902 by King Oscar II of Sweden and Norway, just a year after the award of the first Nobel Prizes. However, plans were dropped as the union between the two countries was dissolved in 1905. As a result, mathematics has never had an international prize of the same dimensions and importance as the Nobel Prize.

Plans for an Abel Prize were revived in 2000, and in 2001 the Norwegian Government granted NOK 200 million (about $22 million) to create the new award. Niels Henrik Abel (1802-1829), after whom the prize is named, was a leading 19th-century Norwegian mathematician whose work in algebra has had lasting impact despite Abel’s early death aged just 26. Today, every mathematics undergraduate encounters Abel’s name in connection with commutative groups, which are more commonly known as “abelian groups” (the lack of capitalization being a tacit acknowledgement of the degree to which his name has been institutionalized).

As it happens, Abel’s own field of group theory plays a role in the Atiyah-Singer Index Theorem, but this is not a condition for the award of the Abel Prize.

The Abel Prize is awarded annually, and is intended to present the field of mathematics with a prize at the highest level. Laureates are appointed by an independent committee of international mathematicians.

As a result of Norway’s action, made in part to celebrate the 200th anniversary of Abel’s birth in 2002, mathematicians now too have an award equivalent to the Nobel Prize. The question is, will the new prize achieve the international luster of a real Nobel? The Nobel Prize in Economics (as it is popularly, but incorrectly, called) achieved that status after it was introduced in 1968, but in that case the Bank of Sweden, which created the award, attached the magic name Nobel to it. (See later.) One could hardly expect Norway to name their prize after a famous Swede, especially when they have Abel to recognize.

Mathematics and the Nobel Prize

Alfred Nobel (1833-1896) made his fortune through the manufacture of explosives. He was born in Sweden, grew up in Russia, studied chemistry and technology in France and the US, and built up companies in several countries all over the world. In his will, Nobel designated the establishment of annual prizes to be given in five areas: Physics, Chemistry, Physiology or Medicine, Literature, and Peace. The prizes are intended to reward specific discoveries or breakthroughs, and the impact of these on the discipline. The first prizes were awarded in 1901. In 1968, a sixth prize was added, in Economics, donated by the Bank of Sweden to celebrate its tercentenary. Strictly speaking, it is not a Nobel Prize but “the Prize in Economic Sciences in Memory of Alfred Nobel.” The Royal Swedish Academy of Sciences selects the prizewinners for physics, chemistry, medicine, literature, and economics, the Nobel Institute at the Karolinska Institute awards the prize in medicine, and the Norwegian Nobel Institute handles the Peace Prize. The monetary amount of each prize varies from year to year. In 2003 it was SEK10 million, about $1.3 million.

Although Nobel did not will a prize for mathematics, over the years many mathematicians have won a Nobel Prize. Taking a fairly generous interpretation for what constitutes being a mathematician, the mathematical Laureates are:

- 1902 Lorentz (Physics)

- 1904 Rayleigh (Physics)

- 1911 Wien (Physics)

- 1918 Planck (Physics)

- 1921 Einstein (Physics)

- 1922 Bohr (Physics)

- 1929 de Broglie (Physics)

- 1932 Heisenberg (Physics)

- 1933 Schroedinger (Physics)

- 1933 Dirac (Physics)

- 1945 Pauli (Physics)

- 1950 Russell (Literature)

- 1954 Born (Physics)

- 1962 Landau (Physics)

- 1963 Wigner (Physics)

- 1965 Schwinger (Physics)

- 1965 Feynman (Physics)

- 1969 Tinbergen (Economics)

- 1975 Kantorovich (Economics)

- 1983 Chandrasekhar (Physics)

- 1994 Selten (Economics)

- 1994 Nash (Economics)

Overall, a fairly good showing for mathematics. Still, this isn’t the same as having a prize for mathematics itself.

A number of theories have been put forward to explain the omission of mathematics from Nobel’s original list. The most colorful suggestion is that Nobel was miffed at mathematicians after discovering that his wife had had an affair with the Swedish mathematician Magnus Mittag-Leffler. Of all the theories, this is the easiest to dismiss, for the simple reason that Nobel never had a wife.

Another oft-repeated suggestion is that Nobel hated mathematics after doing poorly in it at school. It may or may not be true that Nobel wasn’t good at math, but there is no evidence to suggest that a negative high school experience in the math class led to a desire to get back at the mathematicians later in life by not giving them one of his prizes.

By far the most likely explanation, I think, is that he viewed mathematics as merely a tool used in the sciences and in engineering, not as a body of human intellectual achievement in its own right. He also did not single out biology, possibly likewise regarding it as just a tool for medicine, a not unreasonable view to have in the late 19th century.

The Fields Medal

The Fields Medal is often cited as being “the mathematical equivalent of the Nobel Prize.” The Field Medals were first proposed at the 1924 International Congress of Mathematicians in Toronto by Professor J.C. Fields, a Canadian mathematician who was the secretary of the Congress that year. He later donated funds to establish the medals. Fields wanted the awards to recognize both existing work and the promise of future achievement, as a result of which it was agreed to restrict the medals to mathematicians not over forty at the year of the Congress. Medals are awarded every four years, at the Congress, by its organizing body, the International Mathematical Union. Initially, up to two medals were awarded every four years; in 1966 it was agreed that, in light of the great expansion of mathematical research, up to four medals could be awarded at each Congress.

“Fields Medals” are more properly known by their official name, “International medals for outstanding discoveries in mathematics.” The medal is accompanied by a cash prize of CND$15,000.

Atiyah himself received a Fields Medal in 1966.

There are some unique characteristics of the Fields Medal that make it different from a Nobel Prize. First it is awarded only every fourth year. Second, it is given for mathematical work done before the recipient is 40 years of age. Third, the monetary prize that goes with the Fields Medal is considerably less than the Nobel Prize. Fourth, the Fields Medal does not come out of Scandinavia.

When the Norwegian Academy of Science decided to create a prize for mathematics in honor of Abel, they did so with the intention of rectifying what they saw as an omission on the part of Nobel.

The Abel Prize winners

Isadore M. Singer was born in 1924 in Detroit, and received his undergraduate degree from the University of Michigan in 1944. After obtaining his Ph.D. from the University of Chicago in 1950, he joined the faculty at the Massachusetts Institute of Technology (MIT). Singer has spent most of his professional life at MIT, where he is currently an Institute Professor. He is a member of the American Academy of Art and Sciences, the American Philosophical Society and the National Academy of Sciences (NAS). He served on the Council of NAS, the Governing Board of the National Research Council, and the White House Science Council.

Michael Francis Atiyah was born in 1929 in London. He got his B.A. and his doctorate from Trinity College, Cambridge. He spent the greatest part of his academic career at the Universities of Cambridge and Oxford. He was the driving force behind the creation of the Isaac Newton Institute for Mathematical Sciences in Cambridge and became its first director. He was elected a Fellow of the Royal Society in 1962 at the age of 32, and was the Society’s president from 1990 to 1995. He was knighted in 1983 (hence “Sir Michael”) and made a member of the Order of Merit in 1992.

Because of its technical and highly abstract nature of the Index Theorem, it isn’t possible to give a precise statement in a column such as this. The exact formulation requires a heady mix of K-theory, functional analysis, and global analysis. Not long after I got my Ph.D., I met Atiyah in Oxford, and rushed off to read up about his famous theorem. I soon gave up, having decided that life was too short and I had my own mathematical research career to work on.

The press announcement of the award released by the Norwegian Academy of Sciences tried to convey the essence of the result with these words:

“We describe the world by measuring quantities and forces that vary over time and space. The rules of nature are often expressed by formulas involving their rates of change, so-called differential equations. Such formulas may have an “index”, the number of solutions of the formulas minus the number of restrictions which they impose on the values of the quantities being computed. The index theorem calculated this number in terms of the geometry of the surrounding space. … The Atiyah-Singer Index Theorem was the culmination and crowning achievement of a more than 100-year old development of ideas, from Stokes’s theorem, which students learn in calculus classes, to sophisticated modern theories like Hodge’s theory of harmonic integrals and Hirzebruch’s signature theorem.”

Let’s try to get a bit closer to the real thing.

Start with a compact smooth manifold (without boundary) and an elliptic operator E on it. (E is a differential operator acting on smooth sections of a given vector bundle. Laplacians are examples of elliptic operators.) The property of being elliptic is expressed by a symbol s that can be seen as coming from the coefficients of the highest order part of E; s is a bundle section and required to be non-zero. (In the case of a Laplacian, s is a positive-definite quadratic form.) The index of E is defined as the difference between the dimension of the kernel of E and the dimension of the cokernel of E. The “index problem” is to compute the index of E using only the symbol s and topological information about the manifold and the vector bundle. This problem seems to have emerged in the late 1950s. The Atiyah-Singer Index Theorem is its solution.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin (Email: devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and “The Math Guy” on NPR’s Weekend Edition. For a complete list of Math Guy segments, with links, go to http://www- csli.stanford.edu/~devlin/MathGuy.html

Devlin’s most recent book is The Millennium Problems: The Seven Greatest Unsolved Mathematical Puzzles of Our Time, published by Basic Books (hardback 2002, paperback 2003).

MAY 2004

The best popular science essay ever

I became a “math popularizer” almost by accident. In 1983 I had an idea for an April Fools spoof in a national daily newspaper, where I would write a mathematics story that was so counter-intuitive that everyone would think it was a spoof, but the real spoof would be that the story was in fact true. (The story was based on the fact that an engineering company had manufactured a rotary drill that would drill a square hole. To see the mathematics behind this feat, see http://mathworld.wolfram.com/ ReuleauxTriangle.html.)

I wrote it up and sent it in to the science page editor at The Guardian newspaper in my then home country of Britain. A couple of days later the editor telephoned me. He explained to me why my piece would not work in a national newspaper, but went on to say that he liked my writing style, and would be interested in seeing other contributions from me. A few months later an engineer at Cray Research discovered a new record Mersenne prime number, and I wrote a 700 word piece describing the discovery. The editor published it, the reader response was good, and within a short while I found myself a newspaper “math columnist”, with a twice monthly column in the science section.

It wasn’t long before book publishers started to approach me with requests for popular expositions of mathematics. Quite unplanned, I had a second career. Over the years, I have found myself spending more of my time on what has come to be called “public education”, but it remains a very small part of my regular activities. Nevertheless, I have taken it seriously. I read as many popular science books and newspaper and magazine articles about science I can, and I study closely the way the different successful science writers and journalists go about their job.

An essential device in trying to convey mathematics or science to a lay audience is metaphor. The more basic and familiar the metaphor, the greater the audience the writer can reach. To my mind, the queen of the metaphor in science writing is K. C. Cole of the Los Angeles Times. K.C. (as she prefers to be called) has published several collections of her articles from the LA Times in book form, and I recommend them all to anyone who wants to try their hand at science writing for a lay audience.

My all time favorite K.C. Cole piece, which I would claim is the best short newspaper article about science ever, first appeared in her “Mind over Matter” column in the Times on May 11, 2000. (Here on the West Coast we don’t use the initials “LA”, since the New York Times is referred to by its full name.) Titled “Murmurs”, it was republished in K.C.’s book Mind Over Matter: Conversations with the Cosmos, published by Harcourt in 2000 (pp. 15-17). In exactly 700 words (the ideal target length for a newspaper column), using a string of brilliantly conceived everyday metaphors, K.C. succeeds in describing the birth and early development of the universe. Not just describing; she brings it to life. At the same time, she manages to convey the dedication and the excitement of the astrophysics community in their quest to piece together this remarkable story.

With K.C.’s permission, I am reprinting her entire article. There is no special occasion. I just felt this marvellous piece deserved a further spin. I have resisted the temptation to analyze the article paragraph by paragraph, although I have done so for myself and found it well worth the effort. You can dissect it for yourself.

Here then, is what I claim is the best short, lay exposition of science there has ever been.

Murmurs

by K. C. Cole

When the universe speaks, astronomers listen.

When it sings, they swoon.

That’s roughly what happened recently when a group of astronomers published the most detailed analysis yet of the cosmos’s primordial song: a low hum, deep in its throat, that preceded both atoms and stars.

It is a simple sound, like the mantra “Om.” But hidden within its harmonics are details of the universe’s shape, composition, and birth. So rich are these details that within hours of the paper’s publication, new interpretations of the data has already appeared on the Los Alamos web server for new astrophysical papers.

“It’s stirred up a hornet’s nest of interest,” said UCLA astronomer Ned Wright, who gave a talk to his colleagues on the paper—as did so many others—the very next week.

So what is all the fuss about? Why are astronomers churning out paper after paper on what looks to a layperson like a puzzling set of wiggly peaks—graphic depictions of the sound, based on hours of mathematical analysis?

Because there’s scientific gold in them there sinusoidal hills.

The peak and valleys paint a visual picture of the sound the newborn universe made when it was still wet behind the ears, a mere 300,000 years after its birth in a big bang. Nothing existed but pure light, sprinkled with a smattering of subatomic particles.

Nothing happened, either, except that this light and matter fluid, as physicists call it, sloshed in and out of gravity wells, compressing the liquid in some places and spreading it out in others. Like banging on the head of a drum, the compression of the “liquid light” as it fell into gravity wells set up the “sound waves” that cosmologist Charles Lineweaver has called “the oldest music in the universe.”

Then, suddenly, the sound fell silent. The universe had gotten cold enough that the particles, in effect, congealed, like salad dressing left in the fridge; the light separated and escaped, like the oil on top.

The rest is the history of the universe: The particles joined each other to form atoms, stars, and everything else, including people.

“The universe was very simple back then,” said Caltech’s Andrew Lange in one talk. “After that, we have atoms, chemistry, economics. Things go downhill very quickly.”

As for the light, or radiation, it still pervades all space. In fact, it’s part of the familiar “snow” that sometimes shows up on broadcast TV. But it’s more than just noise: When the particles congealed, they left an imprint on the light.

Like children going after cookies, the patterns of sloshing particles left their sticky fingerprints all over the sky.

The pattern of the sloshes tells you all you need to know about the very early universe: its shape, how much was made of matter, how much of something else.

The principal is familiar: Your child’s voice sounds like no one else’s because that resonant cavities within her throat create a unique voiceprint. The large, heavy wood of the cello creates a mellower sound than the high-strung violin. Just so, the sounds coming from the early universe depend directly on the density of matter, and the shape of the cosmos itself.

Astronomers can’t hear the sounds, of course. But they can read them on the walls of the universe like notes on a page. Compressed sounds gets hot and produces hot splotches, like a pressure cooker. Expanded area’s cool. Analyze the hot and cold patches and you get a picture of the sound: exactly how much falls on middle C or B-flat.

What they’ve seen so far is both exciting and troubling. The sound suggests that the universe is a tad too heavy with ordinary matter to agree with standard cosmological theories; it resonates more like an oboe than a flute. Something’s going on that can’t be explained. The answers will come as even more sensitive cosmic stethoscopes listen in over the next few years.

Lest you think these sounds are music only for astronomers’ ears, consider: The same wrinkles in space that created the gravity wells that gave it rise to the sound also blew up to form clusters, galaxies, stars, planets, us.

Even Hare Krishnas murmuring Om.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin (Email: devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and “The Math Guy” on NPR’s Weekend Edition. For a complete list of Math Guy segments, with links, go to http://www- csli.stanford.edu/~devlin/MathGuy.html

Devlin’s most recent book is The Millennium Problems: The Seven Greatest Unsolved Mathematical Puzzles of Our Time, published by Basic Books (hardback 2002, paperback 2003).

JUNE 2004

Good stories, pity they’re not true

The enormous success of Dan Brown’s novel The Da Vinci Code has introduced the famous Golden Ratio (henceforth GR) to a whole new audience. Regular readers of this column will surely be familiar with the story. The ancient Greeks believed that there is a rectangle that the human eye finds the most pleasing, and that its aspect ratio is the positive root of the quadratic equation

x2 – x – 1 = 0

You are faced with this equation when you try to determine how to divide a line segment into two pieces such that the ratio of the whole line to the longer part is equal to the ratio of the longer part to the shorter. The answer is an irrational number whose decimal expansion begins 1.618.

Having found this number, the story continues, the Greeks then made extensive use of the magic number in their architecture, including the famous Parthenon building in Athens. Inspired by the Greeks, future generations of architects likewise based their designs of buildings on this wonderful ratio. Painters did not lag far behind. The great Leonardo Da Vinci is said to have used the Golden Ratio to proportion the human figures in his paintings—which is how the Golden Ratio finds its way into Dan Brown’s potboiler.

It’s a great story that tends to get better every time it’s told. Unfortunately, apart from the fact that Euclid did solve the line division problem in his book Elements, there’s not a shred of evidence to support any of these claims, and good reason to believe they are completely false, as University of Maine mathematician George Markowsky pointed out in his article “Misconceptions About the Golden Ratio”, published in the College Mathematics Journal in January 1992. But with such a wonderful story, which marries some decidedly accessible pure mathematics with aethestics, architecture, and painting—a high school math teacher’s dream if ever there were one—the facts have had little impact.

But being aware that few people will take note of what I say has never stopped me before. (I was, after all, a department chair in a college mathematics department for four years and a college dean for another eight.) So let’s try to separate the fact from the fiction.

First, what do we know for sure about the Golden Ratio? As mentioned above, Euclid showed how to calculate it, but his interest seemed more that of mathematics than visual aesthestics or architecture, for he gave it the decidedly unromantic name “extreme and mean ratio”. The term “Divine Proportion,” which is oten used to refer to GR, first appeared with the publication of the three volume work by that name by the 15th century mathematician Luca Pacioli. Calling GR “golden” is even more recent: 1835, in fact, in a book written by the mathematician Martin Ohm (whose physicist brother discovered Ohm’s law).

It is also true that the Golden Ratio is linked to the pentagram (five-pointed star), to the five Platonic solids, to fractal geometry, to certain crystal structures, and to Penrose tilings. So far so good.

The oft repeated claim (actually, all claims about GR are oft repeated) that the ratios of successive terms of the Fibonacci sequence tend to GR is also correct. The Fibonacci sequence, you may recall, is generated by starting with 0, 1 and repeatedly applying the rule that each new number is equal to the sum of the two previous numbers. So 0+1 = 1, 1+1 = 2, 1+2 = 3, 2+3 = 5, etc., giving the sequence 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, … The sequence of successive ratios of the numbers in this sequence, namely 1/1 = 1; 2/1 = 2; 3/2 = 1.5; 5/3 = 1.666… ; 8/5 = 1.6; 13/8 = 1.625; 21/13 = 1.615…; 34/21 = 1.619…; 55/34 = 1.6176…; 89/55 = 1.6181; …, does indeed tend to GR. As I’ll explain momentarily, this is a key part of the explanation of why the Fibonacci numbers keep appearing in flowers and plants—which they do.

For instance, if you count the number of petals in most flowers you will find that the answer is a Fibonacci number. For example, an iris has 3 petals, a primrose 5, a delphinium 8, ragwort 13, an aster 21, daisies 13, 21, or 34, and Michaelmas daisies 55 or 89 petals. All Fibonacci numbers.

Again, if you look at a sunflower, you will see a beautiful pattern of two spirals, one running clockwise, the other counterclockwise. Count those spirals, and for most sunflowers you will find that there are 21 or 34 running clockwise and 34 or 55 counterclockwise, respectively—all Fibonacci numbers. Less common are sunflowers with 55 and 89, with 89 and 144, and even 144 and 233 in one confirmed case. Other flowers exhibit the same phenomenon; the wildflower Black-Eyed Susan is a good example. Similarly, pine cones have 5 clockwise spirals and 8 counterclockwise spirals, and the pineapple has 8 clockwise spirals and 13 going counterclockwise.

Finally, if you take a close look at the way leaves are located on the stems of trees and plants, you will see that they are located on a spiral that winds around the stem. Starting at one leaf, count how many complete turns of the spiral it takes before you find a second leaf directly above the first. Let P be that number. Also count the number of leaves you encounter (excluding the first one itself). That gives you another number Q. The quotient P/Q is called the divergence of the plant. (The divergence is characteristic for any particular species.) If you calculate the divergence for different species of plants, you find that both the numerator and the denominator are usually Fibonacci numbers. In particular, 1/2, 1/3, 2/5, 3/8, 5/13, and 8/21 are all common divergence ratios. For instance, common grasses have a divergence of 1/2, sedges have 1/3, many fruit trees (including the apple) have a divergence of 2/5, plantains have 3/8, and leeks come in at 5/13.

Although many of these observations were made a hundred year or more ago, it was only recently that mathematicians and scientists were finally able to figure out what is going on. It’s a question of Nature being efficient.

For instance, in the case of leaves, each new leaf is added so that it least obscures the leaves already below and is least obscured by any future leaves above it. Hence the leaves spiral around the stem. For seeds in the seedhead of a flower, Nature wants to pack in as many seeds as possible, and the way to do this is to add new seeds in a spiral fashion.

As early as the 18th century, mathematicians suspected that a single angle of rotation can make all of this happen in the most efficient way: the Golden Ratio (measured in number of turns per leaf, etc.). However, it took a long time to put together all the pieces of the puzzle, with the final step coming in the early 1990s.

The worst kind of angle for efficient growth would be a rational number of turns, eg. 2 turns, or 1/2 a turn, or 3/8 of a turn, since they will soon lead to a complete cycle. Mathematically, a turn through an irrational part of a circle will never cycle, but in practical terms it could eventually come close. What angle will come least close to a cycle? Maximum efficiency will be achieved when the angle is “furthest away” from being a rational. But what exactly does that mean? The appropriate way (via s vis plant growth) to measure how far removed from being rational an irrational number is, is to look at its continued fraction expansion. For GR, this is:

Rational numbers have a finite continued fraction. That unending, constant sequence of 1’s in the continued fraction for GR says that, measured in terms of continued fractions, GR is the irrational number furthest removed from being rational. And that’s the mathematical reason why Nature favors GR as her growth ratio. The Fibonacci numbers appear because the number of leaves, spirals, etc. are whole numbers, and (because of the ratio limit property mentioned above) the Fibonacci numbers are the best whole number approximations to a GR growth.

For other examples of the appearance of the Golden Ratio in Nature, the growth of the Nautilus shell is governed by the Golden Ratio, as is the path followed by a Pergrine falcon when it swoops down to catch its pray. In these cases, the explanation is that the GR is closely related to the logarithmic spiral, the spiral that turns by a constant angle along its entire length, making it everywhere self-similar.

As the Nautilus grows, it has repeated need to enlarge its living quarters. Since the creature does not change shape, rather simply grows larger, the most efficient way to do this is for its shell to grow in the self-similar form of a logarithmic spiral.

The falcon must keep the prey in its sight all the time, but, although its eyes are razor sharp, they are fixed in its head, one on either side. So what the creature does is swivel its head to one side, by an angle of about 40o, and fix the prey in one eye. Keeping its head fixed at that 40o angle, the falcon then dives in a way that keep the prey in view in that one eye. The fixed angle of the head results in the bird following an equi-angular spiral path that converges on the prey.

So much for the good (i.e., true) stuff. Now for those many, many myths about GR that continue to do the rounds. The issue here is not whether you can find GR somewhere. If you look hard enough you will be able to find any (reasonably sized) number almost anywhere. The question is whether there is more to it than mere numerology. Is there a good scientific explanation to show why GR appears (as with the examples from Nature mentioned above), or is there definite evidence that, say, a particular artist made deliberate use of GR in his or her work? If not, all you have is an unsubstantiated belief. You may as well believe in fairies.

First of all, whether or not the ancient Greeks felt that the Golden Ratio was the most perfect proportion for a rectangle, many modern humans do not. Numerous tests have failed to show up any one rectangle that most observers prefer, and preferences are easily influenced by other factors. As to the Parthenon, all it takes is more than a cursory glance at all the photos on the Web that purport to show the Golden Ratio in the structure, to see that they do nothing of the kind. (Look carefully at where and how the superimposed rectangle—usually red or yellow—is drawn and ask yourself: why put it exactly there and why make the lines so thick?)

Another claim is that if you measure the distance from the tip of your head to the floor and divide that by the distance from your belly button to the floor, you get GR. But this nonsense. First of all, you won’t get exactly the number GR. You never can; GR is irrational, remember. But in the case of measuring the human body, there is a lot of variation. True, the answers will always be fairly close to 1.6. But there’s nothing special about 1.6. Why not say the answer is 1.603? Besides, there’s no reason to divide the human body by the navel. If you spend a half an hour or so taking measurements of various parts of the body and tabulating the results, you will find any number of pairs of figures whose ratio is close to 1.6, or 1.5, or whatever you want.

Then there is the claim that Leonardo Da Vinci believed the Golden Ratio is the ratio of the height to the width of a “perfect” human face and that he used GR in his Vitruvian Manpainting. While there is no concrete evidence against this belief, there is no evidence for it either, so once again the only reason to believe it is that you want to. The same is also true for the common claims that Boticelli used GR to proportion Venus in his famous painting The Birth of Venus and that Georges Seurat based his painting The Parade of a Circus on GR.

Painters who definitely did make use of GR include Paul Serusier, Juan Gris, and Giro Severini, all in the early 19th century, and Salvador Dali in the 20th, but all four seem to have been experimenting with GR for its own sake rather than for some intrinsic aesthetic reason. Also, the Cubists did organize an exhibition called “Section d’Or” in Paris in 1912, but the name was just that; none of the art shown involved the Golden Ratio.

Then there are the claims that the Egyptian Pyramids and some Egyptian tombs were constructed using the Golden Ratio. There is no evidence to support these claims. Likewise there is no evidence to support the claim that some stone tablets show the Babylonians knew about the Golden Ratio, and in fact there is good reason to conclude that it’s false.

Turning to more modern architecture, while it is true that the famous French architect Corbusier advocated and used the Golden Ratio in architecture, the claim that many modern buildings are based on Golden Rectangles, among them the General Secretariat building at the United Nations headquarters in New York, seems to have no foundation. By way of an aside, a small (and not at all scientific) survey I carried out myself a few months ago revealed that all architects polled knew about the GR, and all believed that other architects used the GR in their work, but none of them had ever used it themselves. Make whatever inference you wish.

Music too is not without its GR fans. Among the many claims are: that some Gregorian chants are based on the Golden Ratio, that Mozart used the Golden Ratio in some of his music, and that Bartok used GR in some of his music. All those claims are without any concrete support. Less clear cut is whether Debussy used the Golden Ratio in some of his music. Here the experts don’t agree on whether some GR patterns that can be discerned are intended or spurious.

Poetry too is not immune, but here there is a refreshing surprise in store for us. Whereas the claim that the Roman poet Vergil based the meter of his poem Aeneid on the Golden Ratio has no support, it really is true that some 12th Century Sanskrit poems have a meter based on the Fibonacci sequence (and hence related to the Golden Ratio).

I could go on, as there are many more examples, ranging from the sacred (eg. the dimensions of the Ark of the Covenant) to the profane (such as, predicting the behavior of the stock market), all of which, on close examination, turn out to be without any supporting evidence whatsoever. Despite the lack of evidence, however, and in some cases in the face of evidence to the contrary, each claim seems to attract its own band of devotees, who will not for a moment entertain the possibility that their cherished beliefs are not true. Consequently, not only is GR a very special number mathematically—all of its genuine appearances in mathematics and Nature show that—it also has enormous cultural significance as the number that most people have the greatest number of false beliefs about. Now there’s a GR fact that has plenty of supporting evidence.

For more details on the Golden Ratio, including evidence to support many of the claims I have made above, see the Markowsky article mentioned earlier, as well as the excellent book The Golden Ratio: The Story of PHI, the World’s Most Astonishing Number, by Mario Livio. Also worth a visit is Ron Knott’s excellent website Fibonacci Numbers and the Golden Section, at the University of Surrey in England.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin ( devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and The Math Guy on NPR’s Weekend Edition. Devlin’s most recent book is Sets, Functions, and Logic: an Introduction to Abstract Mathematics (Third Edition), published by Chapman and Hall in 2003.

JULY-AUGUST 2004

The Two Envelopes Paradox

I received a letter recently asking for me to “rule” on a debate two people were having about the notorious two envelopes paradox. Since my efforts to convince people of the correct resolution to the Monty Hall Problem inevitably generate a small avalanche of letters claiming I am completely wrong, I have in the past hesitated to tackle the much, much trickier envelopes puzzle. But the time has come, I think, to throw caution to the wind, and enter the fray.

Here, for those unfamiliar with the problem, is what it says.

You are taking part in a game show. The host offers you two envelopes, each containing a check. You may choose one, keeping the money it contains. She tells you that one envelope contains exactly twice as much as the other, but does not tell you which is which.

Since you have no way of knowing which envelope contains the larger sum, you pick one at random. The host asks you to open the envelope. You do so and take out a check for $40,000.

Here is where things get interesting, especially for contestants who know some mathematics.

The host now says you have a chance to change your mind and choose the other envelope. If you don’t know anything about probability theory, particularly expectations, you probably say to yourself, the odds are fifty-fifty that you have chosen the larger sum, so you may as well stick with your first choice. (And you’d be right. But I’ll come back to this in a moment.)

On the other hand, if you know a bit (though not too much) about probability theory, you may well try to compute the expected gain due to swapping. The chances are you would argue as follows. The other envelope contains either $20,000 or $80,000, each with probability .5. Hence the expected gain of swapping is

[0.5 x 20,000] + [0.5 x 80,000] – 40,000 = 10,000

That’s an expected gain of $10,000. So you swap.

But wait a minute. There’s nothing special about the actual monetary amounts here, provided one envelope contains twice as much as the other. Suppose you opened one envelope and found $M. Then you would calculate your expected gain from swapping to be

[0.5 x M/2] + [0.5 x 2M] – M = M/4

and since M/4 is greater than zero you would swap. Right?

Okay, let’s take this line of reasoning a bit further. If it doesn’t matter what M is, then you don’t actually need to open the envelope at all. Whatever is in the envelope you would choose to swap. Still with me?

Well, if you don’t open the envelope, then you might as well choose the other envelope in the first place. And having swapped envelopes, you can repeat the same calculation again and again, swapping envelopes back and forward ad-infinitum. There is no limit to the cumulative expected gain you can obtain. But this is absurd.

And there’s the paradox. What is wrong with the computation of the expected gain from swapping?

The answer is everything. The above computation is meaningless—which is why it leads so easily to a nonsensical outcome. If you want to apply probability theory, you are free to do so, but you need to do it correctly. And that means working with actual probabilities, taking care to distinguish between prior and posterior probabilities. Let’s take a closer look.

As with the Monty Hall Problem, if you really want to analyze the situation, you have to start by looking at the way the scenario was set up.

Let L denote the lower dollar value of the two checks. The other check thus has value 2L. Let P(L) be the prior probability distribution for the choice the host makes for the lower value in the envelopes. (This will affect the entire game. Of course, we don’t know anything about this distribution. But we can see how it affects the outcome of the game. Read on.

When you make your choice (C) during the game, you choose either the envelope containing the lower value (C=lower) or the one that contains the higher (C=higher). As the amounts are hidden from you, you choose entirely at random, with equal probabilities for the two options, so

P(C=lower) = P(C=higher) = 0.5

During the game, the value (V) of the content of the chosen envelope is revealed to be a certain value M. Given this information, what is the posterior probability that the chosen envelope contains the higher or lower value? That is, what is P(C|V=M), the probability that you chose the envelope containing the lower/higher value, given you now know what V is? This is the probability you need in order to compute any expected gain. The correct expected gain calculation is:

(2M)P(C=lower|V=M)+(M/2)P(C=higher|V=M) – M

The paradox above arose because you assumed that

P(C=lower|V=M) = P(C=higher|V=M) = 0.5

Let’s see why this cannot be the case. (In what follows, remember that L, V, C are variables and M is a numerical constant.)

By Bayes’ Theorem:

P(C|V=M) = P(V=M|C)P(C)/P(V=M) . . . (1)

Taking the first of the two cases, where you choose the lower value (V=L), we have

P(V=M|C=lower) = P(L=M)

The second of the two cases, where the chosen envelope contains double the lower value, is

P(V=M|C=higher) = P(L=M/2)

Substituting each of these two identities in to (1) gives

P(C=lower|V=M) = P(C=lower)P(L=M)/P(V=M) . . . (2)

and

P(C=higher|V=M) = P(C=higher)P(L=M/2)/P(V=M) . . . (3)

From (2), P(C=lower|V=M) is the same as P(C=lower) only if P(L=M) is the same as P(V=M). If it is not then in the calculations of expected gain you have used the incorrect probability. Specifically, you have used the prior probability, P(C=lower)=0.5, of choosing the lower value, rather than the posterior probability P(C=lower|V). The same argument works for P(C=higher|V), starting from (3).

Under what circumstances could we have P(L=M) = P(V=M)?

Since P(V=M) must normalize the distribution, we have

P(V=M) = P(C=lower)P(L=M) + P(C=higher)P(L=M/2)

that is,

P(V=M) = 0.5 P(L=M) + 0.5 P(L=M/2) . . . (4)

From (4), to have P(L=M) = P(V=M) we would need P(L=M/2) = P(L=M) for all values of M. This is an infinite uniform “distribution”. But no such distribution exists (it cannot be normalised). Hence it is impossible to have any prior distribution for which P(L=M) = P(L=M/2) is satisfied for all M. As a result there is no posterior distribution for which, given any V, we could have P(C=lower|V) = 0.5.

The result you will get in the game depends on the prior distribution for the amounts in the envelope. For example if the prior distribution P(L) were uniform between 0 and $30,000, and you found $40,000 in the envelope, then you would expect to lose if you swap, whereas if the prior were uniform between $30,000 and $100,000, you would expect to gain.

To summarize: the paradox arises because you use the prior probabilities to calculate the expected gain rather than the posterior probabilities. As we have seen, it is not possible to choose a prior distribution which results in a posterior distribution for which the original argument holds; there simply are no circumstances in which it would be valid to always use probabilities of 0.5.

Devlin’s Angle is updated at the beginning of each month.

Mathematician Keith Devlin ( devlin@csli.stanford.edu) is the Executive Director of the Center for the Study of Language and Information at Stanford University and The Math Guy on NPR’s Weekend Edition. Devlin’s most recent book is Sets, Functions, and Logic: an Introduction to Abstract Mathematics (Third Edition), published by Chapman and Hall in 2003.

SEPTEMBER 2004

A game of numbers

The approach of the 2004 World Series sees the publication of not one but two books on the use of statistics in baseball. By statistics, I don’t mean what most fans seem to think this means, namely collecting and tabulating game stats, but the use of sophisticated mathematical techniques to examine players’ performance and the effectiveness of various plays in depth, to help clubs make hiring and salary decisions, and to decide on game strategy.

Alan Schwartz, a senior writer at Baseball America, has written a book called The Numbers Game, and math professor and former MAA President Ken Ross of the University of Oregon has published A Mathematician at the Ballpark. These books come close on the heels of last year’s bestseller Moneyball, by Michael Lewis, which described how the Oakland As used mathematics to turn itself into one of the most successful teams in the league, despite being one of the poorest. The Schwartz book is a history of the use of statistics in baseball; it fills in a lot of the details that Lewis skipped over in Moneyball. Ross’s book tries to explain the math itself. All the facts in this article are taken from one or more of these three books.

At this point, I need to admit up front that I am not a baseball fan. I attended my first Major League game only this year. Not that I have anything against the game. Just that, growing up in England, baseball looked to me like rounders played by men in pyjamas who seemed to wear very scratchy underpants that required constant adjustment and who had an unusual propensity for spitting.

Still, as Alan Schwartz points out in his book, many thousands of Americans got interested in math by collecting baseball statistics, including some who went on to be professors of mathematics at major universities like Harvard. I may be one of the few people in the world who did it the other way: I have become interested in baseball (to a degree) through math. And in writing about baseball, as I am now doing, I am following in the tradition set by the “father of baseball”: Henry Chadwick.